Emergencies happen, and pet care can get expensive fast. Veterinary costs have risen by 29.5% from 2021 to 2024, with emergency visits often costing anywhere from $100 to over $2,000 – and in severe cases, even exceeding $40,000. Without savings, many pet owners face difficult decisions, including "economic euthanasia", where treatment is unaffordable.

Here’s what you need to know:

- Start with $1,000–$2,000. This covers minor emergencies.

- Save $2,500–$8,000 if you don’t have pet insurance or have multiple pets.

- Senior pets or breeds prone to health issues may require $3,000–$5,000+.

- Common emergencies include poisoning ($250–$6,000), foreign object removal ($1,500–$7,000), and bloat surgery ($1,500–$8,000).

Pro tip: Build your fund slowly by saving $50–$100/month into a high-yield savings account for quick access. Pair this with pet insurance for added peace of mind. Start now to avoid financial stress when your pet needs care the most.

Does Your Pet Have an Emergency Fund? – Daily Pet Tips

Evaluating Your Pet’s Emergency Risks

When it comes to emergencies, the risks your pet faces – and the costs associated with them – can vary widely. Factors like species, breed, age, and health history all play a role in determining what kind of emergencies might arise.

Risk Factors by Pet Type

Small mammals often face dangers that might not be obvious to owners. For instance, chinchillas are highly sensitive to heat and can suffer fatal heatstroke if temperatures climb above 80°F. On the flip side, hedgehogs are at risk if it gets too cold. If temperatures drop below 70°F, they might enter a torpor state, which is similar to hibernation but can be life-threatening. Injuries are another frequent issue – chinchillas can break legs on narrow cage bars, while rabbits, guinea pigs, and other small mammals are prone to falls, compression injuries, or fractures.

Dietary mistakes are also a major concern for small pets. Feeding them high-sugar treats, for example, can lead to severe gastrointestinal problems in herbivores. Dr. Laurie Hess, DVM, Diplomate ABVP (Avian Practice) at the Veterinary Center for Birds and Exotics, explains the danger:

"The difference between humans consuming these foods and our small mammal pets eating them is that even tiny amounts of these items can be fatal to these animals".

Other risks include heavy metal poisoning, which can happen when small mammals chew on electrical cords or ingest old paint. This can result in nerve damage or even organ failure.

Dogs and cats have their own unique emergency profiles. For cats, urinary obstructions are a common and expensive issue, often costing between $1,500 and $3,000 to treat. Dogs, on the other hand, frequently face trauma-related emergencies. On average, emergency visits cost $653 for dogs and $919 for cats. Certain breeds are more prone to specific health problems. For example, older small dog breeds like Cavalier King Charles spaniels, dachshunds, and chihuahuas are at higher risk for Mitral Valve Disease. Treating this condition can be extremely expensive, with mitral clip procedures costing $15,000 and valve replacements potentially reaching $45,000.

In addition to pet type, factors like age and pre-existing health conditions can add to emergency costs.

How Age and Health Affect Emergency Costs

Your pet’s life stage plays a big role in their emergency risks. Puppies and kittens, while generally requiring routine preventive care, are particularly prone to issues like swallowing foreign objects or contracting infections. Adult pets, especially high-energy breeds, are more likely to get into accidents. Meanwhile, senior pets need the most financial preparation for emergencies, as they are more susceptible to sudden health crises caused by chronic conditions like heart disease, organ failure, or neurological problems.

Pre-existing conditions can make emergencies even more complicated – and costly. For example, around 80% of pets develop dental disease by age 3, which can lead to bacteria entering the bloodstream and damaging major organs. Additionally, about 54% of dogs and cats in the U.S. are overweight or obese, increasing their risk for conditions like diabetes and heart disease. These health issues can reduce their lifespan by up to 2.5 years. Purebred pets often come with genetic predispositions that may require specialized surgeries at some point.

As pets age, you’ll also need to factor in end-of-life expenses, which can include emergency stabilization, euthanasia, and cremation. These costs can add up to roughly $1,500.

Average Emergency Veterinary Costs

Understanding the typical costs of emergency veterinary care can help you set a realistic goal for your pet’s emergency fund. Emergency services tend to be pricier because they operate 24/7, rely on specialized equipment, and employ highly trained staff . Most emergency clinics require an upfront deposit and full payment when you pick up your pet, so having immediate access to funds is essential . Let’s break down the specifics of these expenses.

Typical Veterinary Emergency Expenses

On average, an emergency exam costs about $125 for dogs and $121 for cats across the U.S., though prices vary widely – from $105 in Mississippi to $183 in Hawaii.

Here’s a look at common diagnostic and treatment costs:

- Basic diagnostic tests: Bloodwork costs between $80 and $200, X-rays range from $100 to $400, and ultrasounds are priced at $300 to $600. Advanced imaging, like MRIs or CT scans, can exceed $1,500.

- Supportive care: IV fluids typically cost $60 to $95 per bag, while pain medications range from $40 to $80.

Treatment costs can vary significantly depending on the condition:

- Poisoning treatments range from $250 to $6,000.

- Foreign body removal surgeries cost between $1,500 and $7,000.

- Bloat surgery can run from $1,500 to $8,000.

- Cats may face specific issues like urinary obstructions ($1,500–$3,000) or heatstroke ($1,500–$6,000), while wound care alone can cost $800 to $2,500.

Hospitalization costs also add up quickly. A single night of standard care averages $222 to $567, while intensive care ranges from $800 to $1,500 per night. Multi-day stays can climb to $1,500–$3,500 . Dr. Hunter Finn, a veterinarian, sums it up:

"Emergency costs can range from as little as a few hundred to easily a few thousand dollars, depending on the severity of the case".

With such a wide range of prices, it’s easy to see how emergency care can become a financial burden.

What Affects Emergency Veterinary Costs

Several factors influence the cost of emergency care:

- Location: Urban clinics, especially those operating 24/7, tend to charge more than rural clinics where on-call services are often handled by general veterinarians .

- Pet size and treatment complexity: Larger animals require higher doses of medication, and surgeries for dogs typically cost more ($1,800–$5,000) compared to cats ($1,500–$3,000) .

- Severity of the condition: Life-threatening emergencies often involve advanced imaging or consultations with specialists, which can add thousands to the final bill .

PetPlace explains the challenge of estimating costs upfront:

"Emergency vets are generally not required to provide a pricing list up front, and they may not be able to estimate the cost of your pet’s care until they start an exam and see what they’re dealing with".

Understanding these factors can help you better prepare for potential costs and set realistic savings goals for your pet’s emergency care.

How Much to Save for Pet Emergencies

Pet Emergency Fund Savings Guide by Pet Type and Age

It’s essential to set a practical savings goal for pet emergencies based on your pet’s specific needs and circumstances.

Recommended Starting Fund Amount

Experts generally recommend starting with $1,000 to $2,000. This range can cover minor emergencies like vomiting, minor injuries, or allergic reactions. According to Emergency Veterinary Care Centers (EVCC):

"A solid rule of thumb is to save enough to cover the costs of at least one to two major emergencies. For most pet owners, this amounts to around $1,500 to $3,000".

If you don’t have pet insurance, you might want to aim higher. Lindsey Wolko, founder of the Center for Pet Safety, advises:

"Pet owners should set aside at least $2,500-$8,000 if they do not have pet insurance as an emergency fund. A multi-pet household should aim for the higher range".

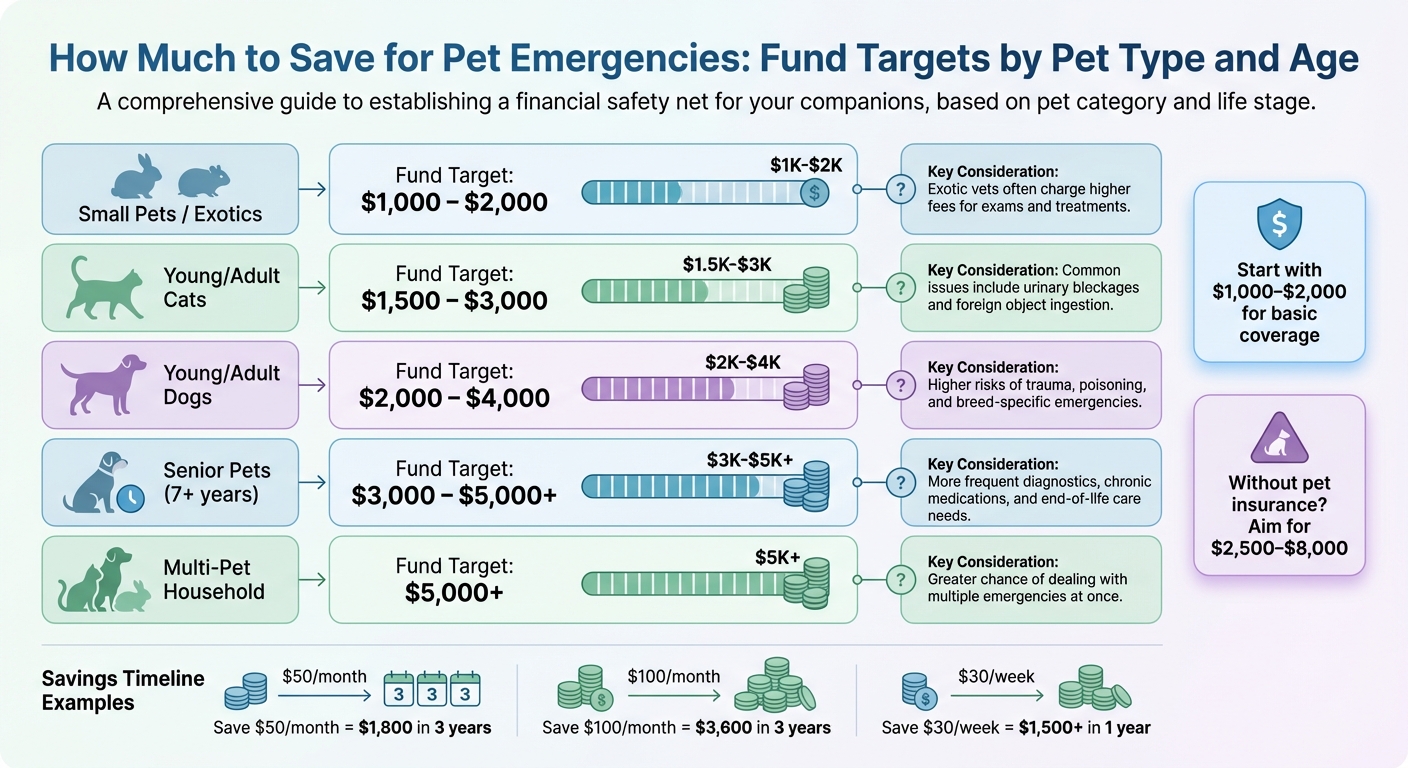

For senior pets – those aged 7 years or older – larger funds are often necessary. Expect to save $3,000 to $5,000 or more, as older pets are more likely to need ongoing treatments, diagnostic tests, and end-of-life care. Similarly, households with multiple pets should aim for $5,000 or more to account for the increased likelihood of simultaneous emergencies.

Fund Targets by Pet Type and Age

Your pet’s type and age can significantly influence your savings target. Here’s a breakdown to help you plan:

| Pet Profile | Recommended Fund Target | Considerations |

|---|---|---|

| Small Pets / Exotics | $1,000 – $2,000 | Exotic vets often charge higher fees for exams and treatments. |

| Young/Adult Cats | $1,500 – $3,000 | Common issues include urinary blockages and foreign object ingestion. |

| Young/Adult Dogs | $2,000 – $4,000 | Higher risks of trauma, poisoning, and breed-specific emergencies. |

| Senior Pets (7+ years) | $3,000 – $5,000+ | More frequent diagnostics, chronic medications, and end-of-life care needs. |

| Multi-Pet Household | $5,000+ | Greater chance of dealing with multiple emergencies at once. |

Breed-specific risks also play a role. For instance, large dogs prone to bloat may require higher savings, as surgery for this condition can cost anywhere from $1,500 to $8,000. Male cats, on the other hand, often face urinary blockages that might cost between $1,500 and $3,000. Researching your pet’s breed can help you identify potential costly conditions and adjust your savings goal accordingly.

Building an emergency fund takes time and commitment. For example:

- Saving $50 per month adds up to about $1,800 in three years.

- Setting aside $100 per month builds approximately $3,600 in three years.

- Even saving $30 a week can grow to over $1,500 in just one year.

Start small if needed, but stay consistent. The key is to begin saving now so you’re prepared when unexpected expenses arise. Up next, explore strategies to grow and maintain your emergency fund.

sbb-itb-e212914

How to Build and Maintain Your Emergency Fund

Effective Ways to Save Money

Automate your pet emergency fund. One of the simplest ways to ensure you’re consistently saving is to set up automatic transfers from your checking account to a dedicated savings account. Schedule these transfers for payday so the money is saved before you’re tempted to spend it. Many employers also allow you to split your direct deposit, making it easy to allocate a portion of your paycheck directly into your pet emergency fund. As Northwestern Mutual explains:

"If you set up an automated transfer each month, you’re saving your money before you even realize it’s there – which means you’re less likely to miss it".

Start with an amount that feels manageable for your budget – perhaps $25 to $50 per month. The key is consistency, not the initial amount. Treat this transfer like a necessary bill. You can also give your savings a boost by adding any unexpected income, such as tax refunds, bonuses, birthday money, or earnings from a side hustle, directly to your fund instead of spending it.

Another helpful tip is to adjust the due dates for your bills to better match your pay schedule. This can create weeks with fewer financial obligations, making it easier to set aside extra cash for savings without feeling stretched. And if you ever need to dip into your emergency fund, make rebuilding it a priority. Resume your regular savings routine as soon as possible to restore the balance.

Once you’ve established a savings habit, it’s time to choose the right type of account to hold your emergency fund.

Where to Keep Your Emergency Fund

Consider a high-yield savings account (HYSA) for your pet emergency fund. These accounts offer competitive interest rates, typically ranging from 3.30% to 5.00% APY as of January 2026, while keeping your money accessible . For instance, if you deposit $5,000 into an account with a 5.00% APY, you’d earn around $256 in interest in a year. Compare that to the national average rate of 0.40%, which would only yield about $22 in the same timeframe.

Separating your emergency fund from your everyday checking account can help you avoid the temptation to spend it on non-essential items . Many digital banks let you nickname your accounts, so consider naming yours something like "Pet Emergency Only" or "Rainy Day Fund" to remind yourself of its purpose. Some banks even offer features like savings buckets or sub-accounts, which can make managing your funds even easier .

Make sure your chosen account is FDIC or NCUA insured to protect your savings . Stay away from certificates of deposit (CDs) for this purpose, as they restrict access to your money and may impose penalties for early withdrawals. Since emergencies require immediate access to funds, HYSAs strike the perfect balance between earning interest and maintaining liquidity.

Pet Insurance and Other Financial Options

How Pet Insurance Works with Emergency Funds

While building an emergency fund is a great first step, pet insurance can provide an additional safety net for your pet’s healthcare needs. Most pet insurance plans require you to pay your vet upfront and then file a claim for reimbursement, which can take up to a month to process.

Pet insurance policies typically revolve around three key components: the deductible (ranging from $100 to $1,000), the reimbursement rate (commonly 70% to 90%), and the annual coverage limit. Your out-of-pocket costs depend on the combination of these factors. Keep in mind that policies often come with waiting periods of a few days to two weeks before coverage begins. Pre-existing conditions, cosmetic procedures, and routine grooming are generally excluded. As of 2024, the average monthly premiums for accident-and-illness policies were $62.44 for dogs and $32.21 for cats.

For context, Embrace Pet Insurance reported its largest individual claim in 2024 – a staggering $41,339 – for a Rhodesian ridgeback treated for pancreatitis and a gastrointestinal ulcer. In such extreme cases, a personal emergency fund of $2,000–$5,000 might not be enough. Amber Batteiger from Embrace Pet Insurance highlights this point:

"One routine vet visit could deplete your entire savings account, depending on where you are in the year. This is why pet insurance is such a valuable option."

To ease the financial burden, some insurers, like Trupanion, offer direct payment options through programs such as VetDirect Pay. This allows veterinarians to be paid directly, leaving you responsible only for the portion not covered by your policy.

Other Ways to Pay for Emergency Care

If your savings and insurance coverage fall short, there are other options to consider. Healthcare financing plans like CareCredit and Scratchpay can help cover emergency expenses. CareCredit functions as a revolving credit account with promotional interest-free periods; however, the standard APR can climb as high as 26.99%. Scratchpay offers short-term loans with repayment terms ranging from 12 to 48 months.

Some veterinary clinics provide in-house payment plans for long-time clients, and many maintain small discretionary "Angel Funds" funded by client donations to assist pet owners facing financial difficulties.

Nonprofit organizations are another resource for financial aid. Groups such as RedRover Relief and The Pet Fund offer grants to qualifying pet owners, while some charities focus on specific conditions like cancer or necessary amputations. Typically, these organizations require a formal diagnosis and an estimate from your veterinarian before reviewing applications.

Crowdfunding platforms like Waggle and GoFundMe can also help. Waggle, in particular, works directly with veterinarians to verify bills and ensures that funds go straight to the clinic, which can inspire confidence among donors. Additionally, veterinary teaching hospitals at universities might offer lower rates for specialized procedures, making them a practical option for complex medical cases.

Conclusion

Setting up a pet emergency fund ensures you’re prepared to handle unexpected medical costs while safeguarding your peace of mind. With one in three pets likely to face emergencies and veterinary expenses climbing by 29.5% between April 2021 and April 2024, the odds of encountering a sudden vet bill are high.

Start by setting a practical savings goal. If you have pet insurance, aim to save $1,000–$2,000 to cover deductibles and co-pays. Without insurance, plan for $3,000–$5,000 – or even $2,500–$8,000 if you have multiple pets. Even small contributions, like $25 to $50 each month, can grow quickly over time. Automating deposits into a high-yield savings account, as discussed earlier, can help you hit these targets efficiently.

More than half of pet owners are financially unprepared for emergencies. Don’t let yourself fall into that category. By having funds readily accessible, you can focus on your pet’s recovery instead of scrambling for payment options or facing the devastating decision between treatment and euthanasia.

Pair your emergency fund with pet insurance if it fits your budget, explore financing options such as CareCredit before you need them, and make it a habit to replenish your savings after any withdrawal. Taking these steps now ensures you’ll be ready to provide the care your pet needs when it matters most.

FAQs

How do I figure out how much to save in an emergency fund for my pet?

To figure out how much to set aside for your pet’s emergency fund, think about factors like their species, size, age, and overall health. For instance, a typical emergency vet visit might cost between $800 and $1,500, while surgeries often range from $1,000 to $3,000. A general guideline is to aim for savings of $1,000 to $5,000, or contribute $50 to $100 per month to build up your fund.

If you have a larger, older, or higher-risk pet, you may need to save more to cover potential emergencies. Being prepared financially means you can tackle unexpected vet bills and ensure your beloved pet gets the care they need.

What are the benefits of having both a pet emergency fund and pet insurance?

Combining a pet emergency fund with pet insurance creates a solid safety net for your pet’s health and your wallet. An emergency fund helps you manage out-of-pocket costs like deductibles, co-pays, or smaller surprise expenses. This way, you’re not forced to rely on credit cards or delay treatment. On the other hand, pet insurance steps in to cover the hefty bills from major illnesses or injuries, which can quickly add up to thousands of dollars.

Together, these tools ease financial worries, letting you focus on what really matters – getting the best care for your pet. By setting aside savings in a dedicated account and choosing a dependable pet insurance plan, you’ll be prepared to tackle both routine vet visits and unexpected emergencies without straining your budget or compromising your pet’s well-being.

What can I do if my pet’s emergency costs more than I’ve saved or my insurance covers?

If a sudden pet emergency stretches beyond what your savings or insurance can handle, the first step is to have a conversation with your veterinarian. Many clinics are willing to provide a detailed breakdown of costs, suggest treating your pet in stages, or even offer payment plans to make the situation more manageable. Be transparent about your financial constraints – they might have solutions or resources to help.

Another avenue to consider is financial assistance programs. Local animal welfare organizations or national charities often provide grants to cover emergency care for pet owners in tough situations. If needed, short-term financing options like a 0% APR credit card or a small personal loan can help cover immediate expenses – just make sure to pay it off promptly to avoid hefty interest charges.

Once the crisis has passed, it’s a good idea to rebuild your emergency fund. Setting aside $50 to $100 each month can help you build up a reserve of $2,000 to $5,000, which is often recommended for pet-related emergencies. Take this time to also review your pet insurance policy to ensure it aligns with your needs, including its coverage limits and deductibles. By taking these steps, you’ll be better prepared to handle unexpected costs down the road.